Dream Bigger. Forge Your Legacy.

Elite Business Strategies for Entrepreneurs Who Refuse to Settle

Insurance Rates Are Skyrocketing!

The Coming Insurance Crisis: What It Means for Homeowners, Business Owners & the Economy

🔥 A Perfect Storm is Brewing in the Insurance Industry

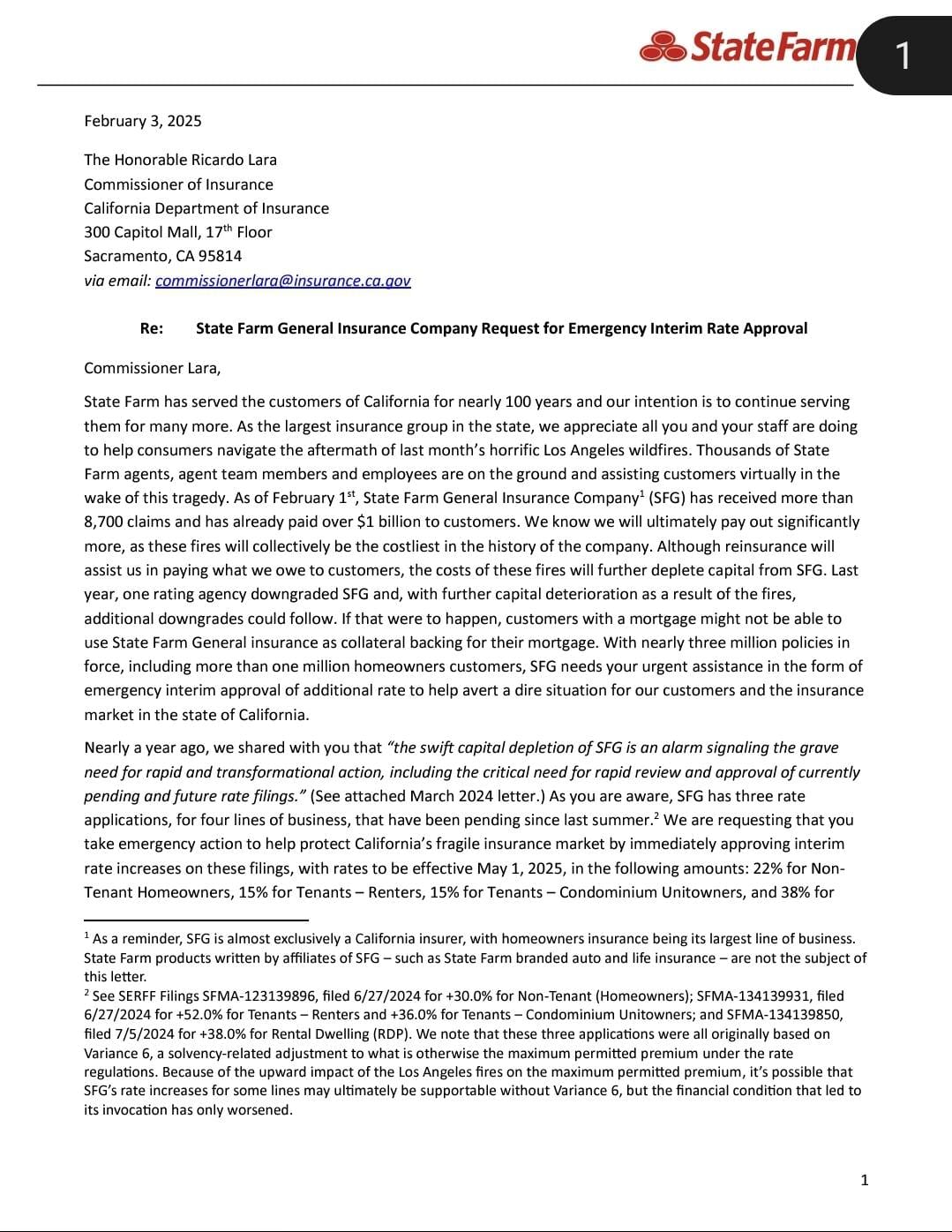

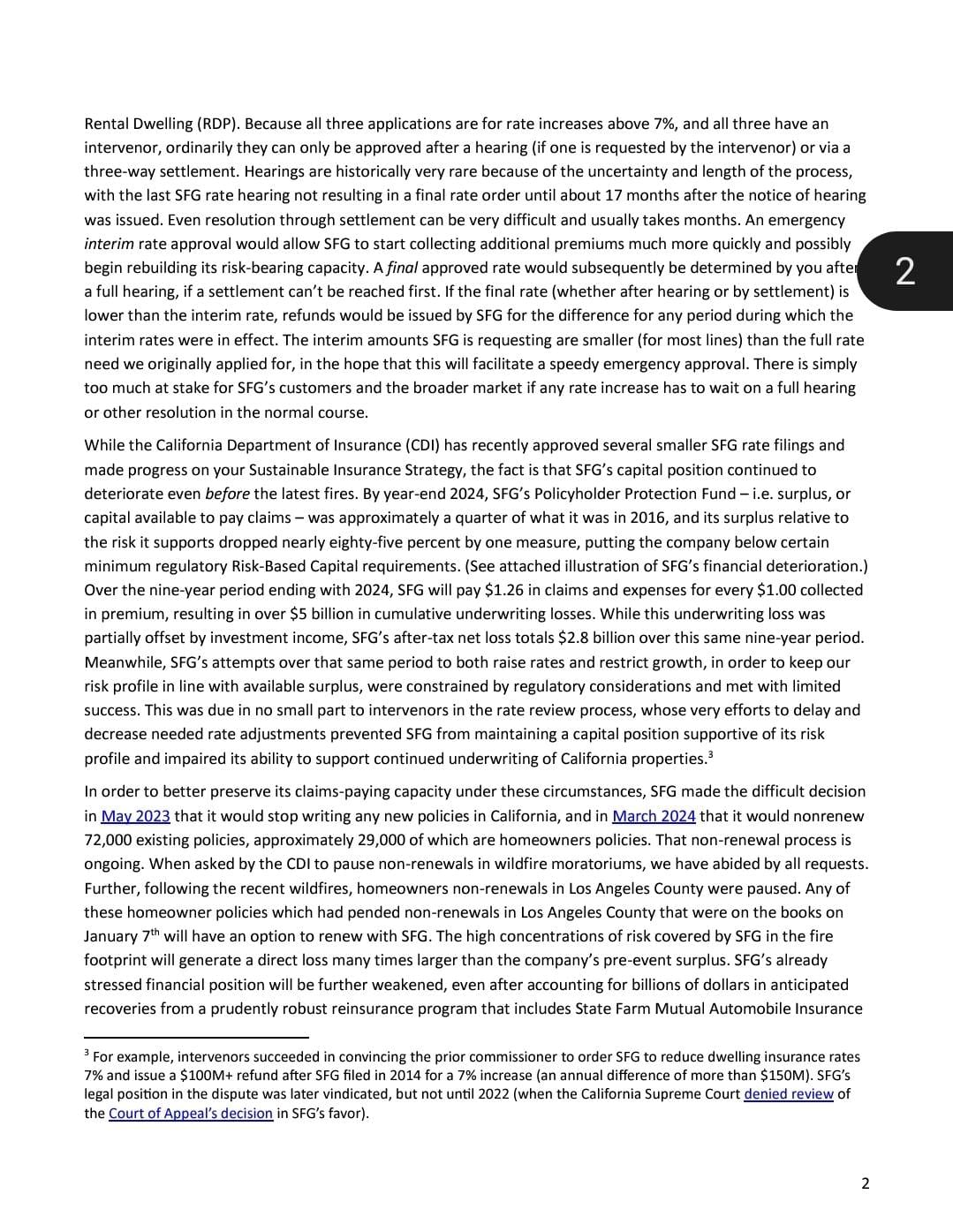

State Farm recently made an urgent plea to the California Department of Insurance, requesting emergency rate hikes following the devastating Los Angeles wildfires. While this might seem like a California issue, the ripple effects could impact homeowners, business owners, and the real estate market nationwide.

The insurance industry is at a crossroads—rising claims, regulatory hurdles, and financial pressures are forcing a fundamental shift in how risk is assessed and how premiums are priced. If you own a home, rent, or run a business, this shift will affect you.

What’s Happening in California?Large Call to Action Headline

State Farm, the state’s largest home insurance provider, has been hit hard by wildfire-related claims. As of February 1, 2025, the company has:

✅ Paid over $1 billion in wildfire claims (and expects to pay billions more).

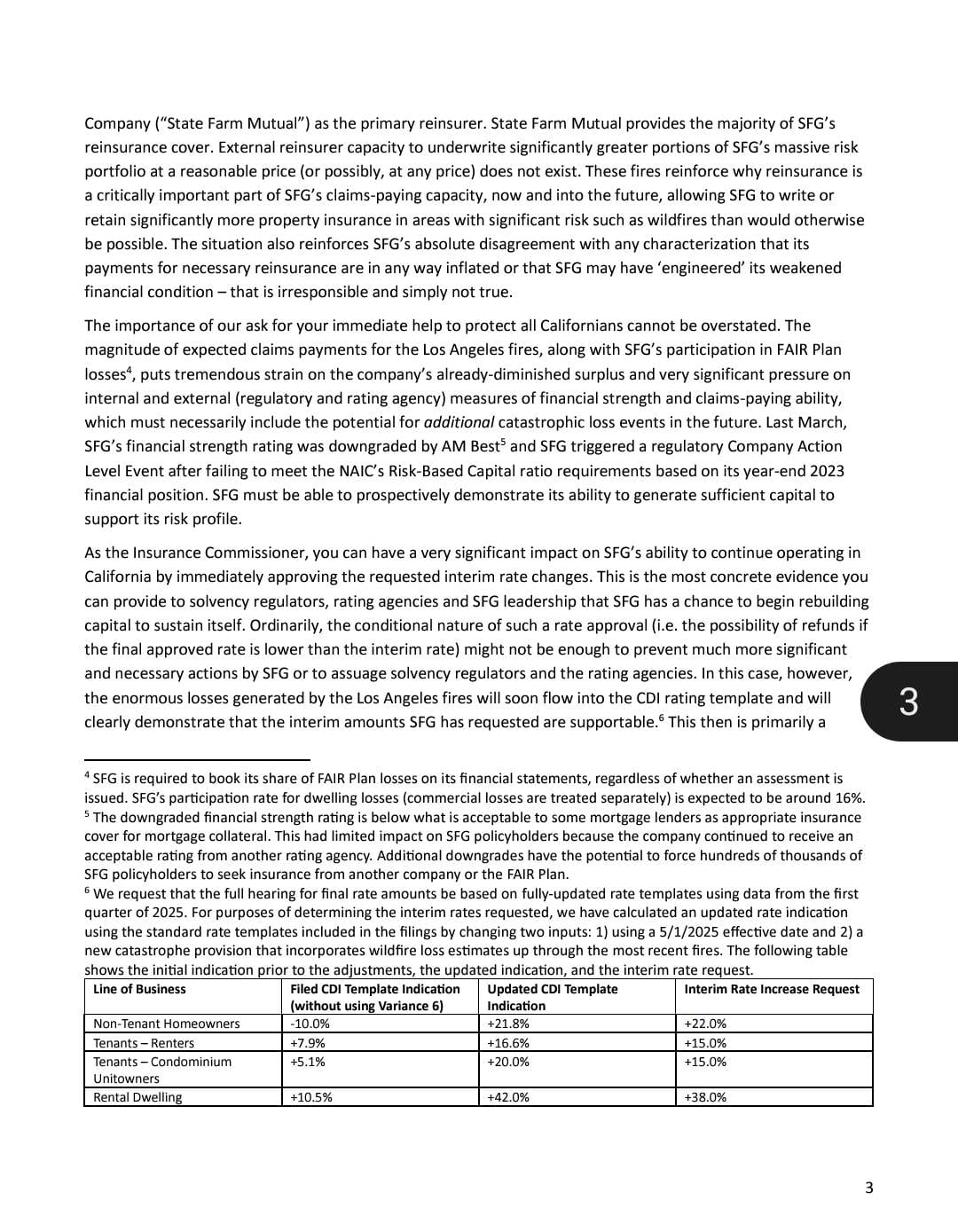

✅ Requested emergency rate increases (as high as 38% for some policyholders).

✅ Stopped issuing new policies in the state (since May 2023).

✅ Dropped 72,000 existing policies (and more may be coming).

✅ Warned that without rate hikes, customers with mortgages may lose their coverage (if lenders stop accepting State Farm policies as valid collateral).

👉 What this means: Insurers are no longer willing to absorb major losses without increasing premiums or exiting risky markets altogether. This shift is already happening in other disaster-prone states.

Why This Matters to You (Even If You’re Not in California)

Even if you don’t live in California, this will impact you. Here’s why:

💰 1. Nationwide Rate Hikes Are Coming

If California approves these emergency rate increases, other states could see similar adjustments.

Hurricane-prone states (Florida, Texas, Louisiana) and Tornado Alley (Midwest, Southeast) will be next as insurers reevaluate risk pricing.

🏠 2. Homeowners May Struggle to Get or Keep Coverage

If State Farm gets downgraded further, mortgage lenders may stop accepting their policies, forcing thousands to seek new insurers.

Other companies may follow suit and pull out of high-risk states, making some properties virtually uninsurable.

This could tank real estate values in disaster-prone regions.

📉 3. Business Owners Could Face Insurance-Related Shutdowns

If commercial policies see massive increases or non-renewals, small businesses may be forced to operate without insurance or shut down.

Liability, flood, and property insurance costs could skyrocket, adding financial strain to businesses across industries.

🔍 4. The FAIR Plan (Insurer of Last Resort) Could Collapse

The California FAIR Plan is already overloaded—if private insurers continue pulling out, more homeowners will rely on this state-backed insurer.

This would increase costs for all policyholders since the FAIR Plan is funded by assessments on all insurance companies.

How to Protect Yourself From Rising Insurance Costs

With the industry shifting rapidly, being proactive is the best defense. Here’s what you can do:

✅ 1. Review Your Current Policy Before Your Next Renewal

Check if you have replacement cost coverage or just actual cash value (ACV policies pay less).

Look for hidden exclusions or new restrictions.

✅ 2. Consider an Independent Insurance Broker

Captive agents (like those from State Farm or Allstate) can only offer their company’s policies.

An independent broker can shop multiple companies to find the best deal.

✅ 3. Take Steps to Reduce Risk (and Qualify for Discounts)

If you live in a wildfire zone, consider fire-resistant upgrades

In hurricane-prone areas, reinforce your roof, windows, and doors.

Many insurers offer discounts for proactive risk reduction.

✅ 4. Understand Your Lender’s Insurance Requirements

If your mortgage lender stops accepting your insurer, you could be forced into an expensive policy (often 2-3x higher in cost).

Make sure your policy meets lender guidelines now to avoid surprises.

✅ 5. If You Own Rental or Investment Property, Reassess Now

High-risk areas may become uninsurable. If insurance companies pull out, property values could drop significantly.

Investors should factor in potential rate increases when evaluating deals.

The Insurance Model is Changing – Are You Ready?

This crisis isn’t just about one wildfire or one rate hike—it’s a fundamental shift in how insurers operate. The traditional insurance model of low, predictable premiums is disappearing in disaster-prone areas.

If you’re a homeowner, business owner, or investor, the time to prepare is NOW. Review your policies, explore your options, and stay ahead of these industry changes before they hit your bottom line.

📚 References & Sources Used in Our Analysis

📄 State Farm’s February 3, 2025 Letter to California’s Insurance Commissioner (Official document outlining requested rate hikes and financial concerns)

📊 State Farm’s Financial Deterioration Report (Includes loss ratios, reinsurance impact, and policyholder effects)

🏠 California FAIR Plan Overview (Details on California’s last-resort insurance option for homeowners)

📉 NAIC Risk-Based Capital Standards (How insurance company financial health is regulated) ⚖️ Recent Court Rulings on California Insurance Regulations

Your source for customized luxury consulting, Workflows & SOPs.

708-606-5856

RoofRiderAcademy@gmail.com

Created with © systeme.io

Privacy policy | Terms of use | Cookies